Confronted with ever-rising European and national climate ambitions, Luxembourg’s industrial community would like to discuss the decarbonisation potential of hydrogen for the industrial- and other adjacent sectors. The discussion focuses on the main application areas where hydrogen could accelerate the decarbonisation, and it sheds light onto how hydrogen can be sourced and at what costs. Further, it tries to find out what could be an approach to introduce hydrogen stepwise in the industrial ecosystem. Finally, it discusses the implications for Luxembourg’s energy policy to create the necessary conditions for hydrogen to make an economically viable contribution to decarbonising the local industry.

Application areas for hydrogen (H2)

This chapter explores three industrial application areas that seem to be most appropriated to deploy hydrogen as carbon neutral alternative fuel. At the same time, it discusses the challenges and possible solutions for such a deployment to materialise.

In the manufacturing sector

In the industrial sector, H2 may solve the decarbonisation of high-temperature processes. H2 can be considered as an alternative fuel in most industrial application, where natural gas cannot be easily substituted by other, less costly and more abundant forms of green energy, above all biomass or renewable electricity. Industrial applications where the latter two sources of renewable energy do not qualify are processes that require temperatures at around 1000 degrees Celsius and above over a persistent time. In Luxembourg’s industry, examples are in glass production, steel- and aluminium re-melting and roller milling, cement production, and the regeneration of catalysts from the petrochemical industry. For none of those industrial processes, however, there already exists an economically viable industrial-scale H2 based alternative technology.

Case: Luxembourg’s steel industry

Luxembourg’s steel industry switched already some 25 years ago from integrated steelmaking in blast furnaces to the re-melting of secondary raw material in an electric arc furnace. Re-melting of recycled steel in electric arc furnaces is 75% less carbon-intensive then integrated steel making which relies on large volumes of coal.

The remaining two direct sources of carbon emissions in re-melting recycled steel by an electric arc furnace are the added foaming coal and the natural gas. Foaming coal is necessary to increase the quality of the electric arc within the oven. It has a direct impact on the latter’s energy efficiency (EE). Natural gas helps heating the oven as well as the semi-finished materials before and during the rolling mill process. If hydrogen could substitute about 20% of the natural gas consumption in rolling mills and if a carbon-neutral agent could completely replace foaming coal without compromising on EE, Luxembourg’s overall national carbon footprint[1] would improve by 0.6%[2].

All the technologies mentioned above, such as compatible hydrogen burners for heat production and foaming coal substitutes are far from being ready to be deployed at an industrial scale. They require substantial efforts and investments in research, development and innovation.

It is worth noting that some volumes of hydrogen are already being used today in Luxembourg’s manufacturing industry. These volumes are consumed as part of industrial processes and not an alternative fuel. Typical examples are in the float glass production, or in galvanisation processes.

In the transport sector

In the transport sector, H2 can reduce CO2 emissions of long-distance mass-passenger and goods transports, e.g. busses, coaches, trucks and lorries. Two different application areas can be foreseen:

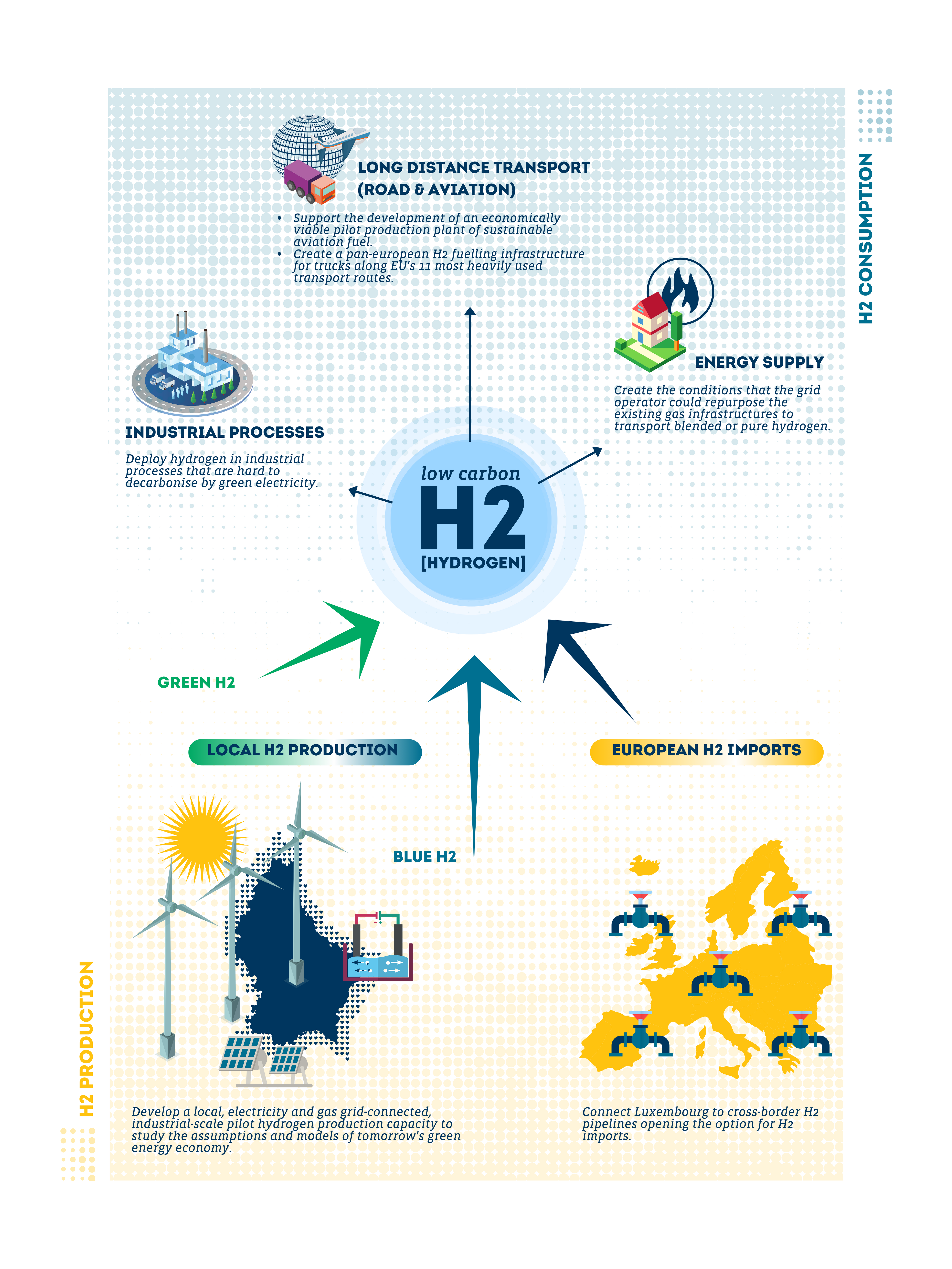

In road transport: H2 as an alternative energy storage medium for long-distance, heavy-duty road transport in vehicles. In the long-distance, heavy-duty road transport sector, battery-powered electric vehicles (BEV) are currently not affordable to the masses. Virtually no offer exists for long-haul, heavy-duty goods transportation as their cost-performance ratios must yet be improved. H2 can thus directly be used in the electric vehicle as storage for green energy to run the vehicle’s fuel cells. Such a decentralised use of H2 in fuel cell vehicles is, however, currently challenging for two reasons. Firstly, there is no comprehensive H2 fuelling infrastructure network across Europe, and secondly, there is no serial-production of affordable fuel cell-powered long-distance mass-passenger or heavy-duty goods transport vehicles. Both challenges could, however, be addressed through an EU initiative by first installing minimal hydrogen fuelling infrastructure along the nine-principal pan-European road transport corridors as defined by the TEN-T Core Network Corridors[3]. Let’s simplify and assume that each of these corridors is about 1000km long and that a hydrogen vehicle can run about 1000km on a charge. The minimum theoretically number of H2 fuelling stations across the EU would only be nine stations. On the long term, the density of a fully-fledged H2 fuelling grid along the EU corridors would probably come close to the number of main fuelling stations designed for truck traffic as they exist today. Still, the coordinated development of such a grid does not seem be out of reach on an EU-27 level in financial terms.

Once an H2 fuelling network is in place, vehicle manufacturers and transport companies can then be incentivised to switch to fuel cell vehicle production. Transport companies can be incentivised to invest in those vehicles by a competitively priced offer of H2 across Europe.

Case: Luxembourg’s transport sector

Luxembourg’s CO2 carbon footprint in the transport sector could be reduced by around 5.2% if 35%[4] of the all the diesel sold to trucks and heavy-duty lorries on the country’s eight highway fuel-stations would be substituted by green hydrogen.

In aviation: H2 to produce synthetic fuel for the aviation industry by capturing CO2. H2 can be used as a source to produce synthetic gas for use in the aviation industry after refining it into proper jet fuel. Such sustainable aviation fuel (SAF) represents the benefit that it reuses CO2, for example, CO2 captured from an industrial installation, to produce the synthetic gas. Even though the combustion of synthetic fuel is not free of CO2 emissions, it does not add new CO2 to the atmosphere if it is produced from an atmospheric source of CO2 in combination with green hydrogen and using renewable electricity for the process. Adding such sustainable aviation fuel (SAF) to kerosene would thus contribute to reducing the CO2 footprint of the aviation sector.

Currently, there is still no installation in operation that could deliver the quantities of SAF necessary to make a notable positive environmental impact. A pilot project in Luxembourg could, therefore, confirm our country’s ambition to take a leading role in the fight against climate change. For the moment, only KLM, the Dutch airline, announced in 2019 a project together with the company called SkyNRG to build a plant that is expected to produce 100,000 tonnes of SAF annually. KLM committed to taking 75,000 tonnes a year for ten years. So far, however, no project roadmap could be found that confirmed the realisation or start of the project.

Case: Luxembourg’s aviation sector

Currently, the best performing SAF can be blended to conventional kerosene up to 50% without significant changes on the jet engine. Under this assumption, Luxembourg could reduce its overall carbon footprint by 5.5% (based on consumption data of 2018, STATEC). In the scope of such a project, Paul Wurth can bring-in its experience as a general contractor and can be responsible for the overall project coordination, the overall plant concept and process integration. This is a competence the company is currently demonstrating within the context of the project Norsk eFuel[5].

In the energy sector

In the energy sector: H2 can also be injected in limited quantities, between 5% to 20%[6]; [7] hydrogen blend by volume, into the natural gas transmission and distribution grids. Despite the limited volumes for reasons of safety, risk of leakage, compatibility with end-users, the integrity of pipelines, etc., this possibility gives access to the large transport and storage capacities of the existing gas grids. Such an injection would thus mean that depending on the compatibility of end-users, green H2 could decarbonise up to 20% of the natural gas used.

Case: Luxembourg’s energy sector

If all end users could still operate with a level of 20% H2 in the gas grid, Luxembourg’s overall carbon footprint could be reduced by 3.6%[8] out of which 1.6%[9] would be realised by the 50 largest industrial natural gas consumers.

Sources of hydrogen

Hydrogen is the most abundant chemical element on earth, but it is rarely found in its pure form in nature. For its use in industrial applications, it must, therefore, be synthesised. The present chapter discusses several methods of hydrogen production and whether they make sense to deploy in Luxembourg to provide hydrogen for local industrial use.

Green hydrogen production by local renewable energy

Hydrogen synthesised for decarbonisation is ideally produced by using renewable energy, e.g. renewable electricity. Such carbon-free synthesised hydrogen is also referred to as green hydrogen. The most straight-forward process is water electrolysis technology. Commercially available electrolysers today deliver energy efficiencies of around 60-80%[10]. In other words, the energy value of the hydrogen produced is about 60-80% of the electricity used to split the water molecule. This hydrogen can then be stored and re-electrified when needed either in fuel cells with efficiencies up to 60%, or it can be burned in combined cycle gas power plants again with similar efficiencies. Alternatively, hydrogen can be used for a thermal process where its efficiency is about 70%.

The above numbers show that there is a loss of about 40% of the energy when transforming electricity into hydrogen via current electrolysis technology. It is thus often considered more efficient, economically viable and ecological to use renewable electricity directly to inject it into the grid than to accept losing so much of it in transformation.

The production of hydrogen via renewable electricity is considered most economically and energetically sensible if there is an excess of renewable electricity on the market, i.e. when the market offer for electricity is higher than demand. This scenario typically happens when, for example, meteorological conditions are favourable for wind- and photovoltaic electricity generation and at the same time, overall demand for electricity is low. Today, renewable electricity generators halt production in this scenario as the price of electricity turns negative, penalising further injection into the grid. Instead of stopping production, wind generators and PV installations could divert the excess electricity to produce hydrogen until the price turn positive again. This process is also referred to as „power-to-gas“, using hydrogen gas as a storage medium for renewable energy.

Data about Luxembourg’s direct-marketing renewable electricity installations show that negative electricity prices represent less than 2% of the potential annual production volumes. They could deliver less than 3 GWh of electricity per year. With the increasing installation of renewable electricity generation capacity, there is also a tendency towards increasing volumes of such lost- or excess renewable energy to produce H2. Nevertheless, the current volumes would need to increase more than 2000 fold to replace the fossil fuels required for a significant reduction of Luxembourg’s carbon footprint[11].

Alternative sources of hydrogen production

As there is not enough excess renewable electricity available in Luxembourg to produce green hydrogen cost-effectively today, we suggest exploring other alternatives. The following two possibilities of hydrogen production, to a certain extent considered as local, may be envisaged:

- By using electricity from the grid in electrolysers – „Grey“ hydrogen

Using electricity from the grid to produce hydrogen represents a theoretical possibility, but in practice, it is difficult for such a production to become economically viable. Too many inefficiencies and would add up: in electrolysis, in the grid, and in electricity generation. Furthermore, as most of the time, electricity from the grid has embedded[12] CO2, the resulting hydrogen cannot be considered a green alternative to fossil fuels. It is therefore also referred to as grey hydrogen and should, for the time being, not be regarded as a sensible source to produce hydrogen for decarbonisation purposes.

- By natural gas reforming with CCS – „Blue“ hydrogen

Currently, over 95% of the global hydrogen production is done via natural gas reforming. Natural gas contains methane (CH4). This methane is used to produce hydrogen via thermal processes, such as steam-methane reformation and partial oxidation. These processes, however, release CO2; steam methane reforming, for example, releases nine to 12 tonnes of CO2 for every tonne of hydrogen produced. If hydrogen is supposed to be an alternative for natural gas in industrial application, it does make sense to substitute it by hydrogen produced from that same natural gas. Energetically, economically and ecologically, this approach does not seem sustainable.

What is intuitively evident for industrial applications does not change much if we would use hydrogen from gas reforming to power transport vehicles or aeroplanes. Even though for an equal amount of energy, CO2 emissions of diesel or jet fuel and natural gas are almost identical, the energy used to transform gas into hydrogen makes the resulting hydrogen’s carbon footprint – at an equal amount of energy – higher than if we use the energy content of diesel or jet fuel right away.

Still, natural gas reforming can be an alternative to substitute fossil fuels by hydrogen if the released CO2 during the process is capture by a CCS/CCU technology and if both processes, reforming and carbon capturing are powered by renewable energy sources. Such hydrogen that meets the CO2 threshold is also referred to as blue hydrogen. Capturing CO2 will substantially increase the cost of natural gas reforming. It will, in turn, allow H2 producers to avoid carbon pricing systems and might, thus, justify the additional costs.

Bearing in mind that for Luxembourg, green hydrogen production is nearly impossible due to the insufficient capacity of installed renewable energy, blue hydrogen could be the next best and most promising alternative[13].

Hydrogen imports

Since the production of green and blue hydrogen in Luxembourg is either not economically viable or politically blocked, the last alternative for Luxembourg to source hydrogen as a fossil fuel substitute is by importing it. For imports of large volumes to be economically viable on the long-term, Luxembourg must consider developing cross-border hydrogen pipeline connections via a dedicated infrastructure with its neighbouring countries, ideally via repurposing its natural gas grid. The creation of such a gateway to access hydrogen imports would open most of the options for its local use as described in the above chapter. It could be injected as a blend into the gas grid, provided as a fuel to the road transport sector or used to produce large quantities of sustainable aviation fuels.

Transport and distribution within Luxembourg should ideally be implemented through a dedicated part of the existing gas grid repurposed for the use of hydrogen. Such repurposing would have the double benefit to create a new low-carbon infrastructure while avoiding stranded assets by phasing-out natural gas as announced by the government.

Currently, the interregional hydrogen pipeline project between France and Germany called „mosaHyc“would offer Luxembourg the possibility to connect to a cross border H2 transportation network. The project between the companies Creos Deutschland GmbH and GRTgaz SA makes a case for repurposing an existing natural gas grid. It shall become a cross-border regional network for the transportation and distribution of unblended hydrogen between Germany, France, and arriving at the Luxembourg border aiming to promote the use of hydrogen as an energy and fuel source in the Saar-Lor-Lux region.

Luxembourg must try to maximise the benefits of this project; it contributes to the development of a hydrogen ecosystem across the three countries. Being connected to a European hydrogen grid represents an enabler for the economy to take advantage of the related green growth opportunities.

Required volumes of hydrogen

The partial decarbonisation of Luxembourg’s industry using green hydrogen would need consequent volumes of the carbon-neutral fuel. If 35% of road transport fuel, 50% of aviation jet fuel and 20% of the natural gas were substituted by green hydrogen, a total annual energy value of over 6900 GWh of hydrogen, or 172’500 tonnes, would be needed[14]. Furthermore, the production of that 6900 GWh of green hydrogen would require over 9100 GWh of renewable electricity. This amount of renewable power is quickly put into perspective by Luxembourg’s total electricity consumption of 6600 GWh in 2018 or the 347 GWh of renewable electricity produced by Luxembourg’s wind and solar installations in that same year[15].

Those numbers show that the use of hydrogen in Luxembourg’s economy can hardly be satisfied by local production. A cross-border grid connection for the import or other means of sourcing of green or blue hydrogen must thus be considered.

The relatively large volumes of hydrogen needed by Luxembourg as described earlier in this chapter give an idea about the enormous quantities that will be necessary for hydrogen to make an impact on Europe’s decarbonisation agenda. Further, against the background of the above-forecasted production volumes, it becomes apparent that massive efforts are required on the short-term to increase the European hydrogen production capacity. Hydrogen production, transmission and distribution must, therefore, receive more considerable attention in the EU industrial strategy, the EU green deal and the EU recovery plan.

Hydrogen Prices

The costs of green hydrogen have been generally considered too high for broad industrial use. Renewable hydrogen as an alternative for fossil fuels is thus still considered economically unviable by many.

The ongoing sharp decline in the cost of renewable energy, in particular of wind power, and also the related perspective of increasing temporarily available excessive offer of renewable power could, however, change the maths behind renewable hydrogen production. The latest research suggests that renewable hydrogen is already cost-competitive in niche applications today. Technology advances combined with expected changes in carbon prices and subsidies can make it competitive already within the next 10 to 15 years, also for large-scale industrial users.

One of the most relevant and widely discussed papers is called: „Economics of converting renewable power to hydrogen“ and was published in Nature Energy[16]. Its two authors analyse the investor’s perspective of a hybrid energy system that combines renewable power with an efficiently sized power-to-gas facility. The authors base their model’s conclusion about a competitive, industrial-scale use of hydrogen mainly on the three following reasons:

- Improvements in electrolysers. The paper makes a performance/cost review of a wide variety of electrolyser technologies. It concludes that both technologies, the one used to convert electricity and water to hydrogen but also the one used for the conversion of hydrogen back to electricity, have improved significantly. In other words, the involved costs have fallen substantially.

- Realtime plant optimisation. Fluctuating prices of renewable electricity on the market are met by a dynamic, realtime decision about whether to sell electricity to the grid or to use it to produce hydrogen. The investment project can be further improved if such a system is installed in a capacity optimised plant. In other words, a plant that is custom made to fit the local wind conditions best to expect for both the renewable source and the power-to-gas electrolysis facility.

- Decreasing costs of wind energy. The study assumes that the investment for installing new wind turbines falls by 4% per year, roughly halving until 2030. It also expects theircapacity factor– an indicator for the actual electricity produced compared to the maximum possible – to increase by 0.7% per year.

Based on the above main assumptions, the model calculates green hydrogen production costs for Germany of $3.23/kg, which are expected to fall to $2.5/kg within a decade.

Currently, however, the above costs must compete with steam methane reformed, grey hydrogen, whose costs are falling under $1/kg even with a relatively high natural gas price of $3.5/MMBtu. The costs to transform this grey hydrogen into a blue one by adding carbon capture will increase the costs to a still competitive $1.4/kg when compared to green hydrogen[17].

The above calculations do not consider the cost of transporting, storing and distributing hydrogen. They usually make-up for more than half the costs of off-grid hydrogen supply. They show, however, that the short to medium term creation of a hydrogen ecosystem can only be successful by deploying the more cost-competitive blue hydrogen first. Preferring to wait until green hydrogen becomes cost-competitive before starting to move may risk missing the window of opportunity for a successful and cost-effective head start.

Policy implications for the promotion of hydrogen as a low carbon fuel

According to the arguments in the previous chapters, hydrogen can indeed play an essential role in contributing to the decarbonisation of industrial applications. FEDIL estimates that a deployment of a 20% hydrogen blend by volume injected into the national gas grid, its use to substitute parts of the kerosene in aviation by synthetic fuels and its partial substitution of diesel in the road transport sector could improve the overall national footprint by over 14%[18]. On the mid-term, complete substitution of diesel by H2 in the route transport sector would even enhance the national carbon footprint by 25%.

The above estimations about national hydrogen demand and its costs are based on assessments and discussions among a limited number of local energy experts. They will undoubtedly need further refinement and should not be taken as the ultimate wisdom. A more profound and broader discussion is necessary to allow modelling how demand and offer of hydrogen across all relevant sectors can be expected to evolve in the future. Such a national hydrogen agenda must involve public and private sector stakeholders and should yield data about how demand articulates, in terms of volumes, geography and timing, and how the offer and corresponding infrastructure can be set-up accordingly.

Nevertheless, the present discussion identified clearly that the volumes of hydrogen required to decarbonise the economy significantly could not be all produced locally. One precondition to consider hydrogen as an alternative fuel at all is, therefore, to secure cross-border sourcing. A potential solution would be a cross-border H2 pipeline interconnection enabling hydrogen imports. A repurposing of the existing natural gas grid for the transport and distribution of the new fuel should also be considered.

Finally, our discussions showed the massive need for efforts in research, development, innovation and market-acceptance as in most sectors, green hydrogen solutions are not yet ready. Most obviously, solutions are needed to substitute natural gas in many energy-intensive industries, diesel in goods and mass-passenger road transport and kerosene in the aviation industry. But also, efficiency improvements of industrial-scale electrolysers as well as competitively priced renewable electricity are necessary to bring the price of green hydrogen production further down.

Policymakers must consider the following points to achieve some short term and yet notable decarbonisation gains using hydrogen:

- Support gas grid operators, including other potential stakeholders to engage in projects that connect Luxembourg to cross-border H2 pipelines opening the option for H2 imports with real benefits for Luxembourg’s decarbonisation goals. It is thus important for Luxembourg to seize the opportunity to directly participate in the project „mosaHyc“described in chapter 3.

- Create the conditions that the grid operator could adapt and repurpose the existing gas infrastructures in Luxembourg for a mid- and long-term use of transporting either blended or pure hydrogen. This approach would also allow avoiding stranded investments in existing gas infrastructures.

- Use imported, cost-effective blue hydrogen in a short to medium term to promote the pick-up of a local hydrogen ecosystem and to test the related economy. The deployment of blue hydrogen must be part of a long-term roadmap that gives green hydrogen the time to become cost competitive.

- Incentivise the development of a local, electricity grid-fed, industrial-scale pilot hydrogen production capacity connected to the gas network. The deployed hardware should use a hybrid energy system that combines efficiently sized renewable power generation with a power-to-gas facility. This pilot project shall contribute to verify and optimise assumptions and models of the green energy economy of the future while providing low carbon fuel to some dedicated industrial actors.

- Review the government’s initial position on not supporting any CCS/CCU initiatives and the non-deployment of CCS/CCU projects in Luxembourg. Luxembourg should consider investing in Pan-European CCS/CCU infrastructure projects to help to accelerate the deployment of blue hydrogen further.

- Support the development of an economically viable pilot production plant of sustainable aviation fuel (SAF) between local technology providers and the national passenger and freight airlines for the gradual decarbonisation of the aviation industry.

- Initiate and animate a national hydrogen agenda allowing to match demand and offer of H2. This agenda should allow breaking-out of the chicken and egg dilemma so typically associated with the market introduction of new technologies. Involve the community of energy-intensive industries to develop an investment agenda for the implementation of the hydrogen infrastructure described in points 1-5. This initiative should be entrusted as a formal mission to an independent body in proximity to the government as part of the National Energy and Climate Plan’s implementation.

- Advocate on the EU level to focus Horizon Europe RDI programmes to work on solutions to decarbonise energy-intensive industries using hydrogen and to develop them beyond laboratory scale to near industrial scale.

- Advocate on the EU level to create an H2 fuelling infrastructure along the most heavily used transport routes and in parallel incentivise vehicle manufacturers to develop H2 powered drive train technologies for heavy-duty, long-haul transport vehicles.

- Review EU grid remuneration rules to allow upfront investments into grid development that is backed by the government. If today such investments were to be done by the grid operator alone, the latter could rapidly face cash flow problems as the massive short-term upfront investments would only be reimbursed over a very long period via the grid usage fees of the consumers connected to it.

- Strengthen, sharpen and promote the participation of Luxembourg in existing European initiatives and tools such as the Clean Hydrogen Partnership, the Hydrogen IPCEI, the Hydrogen Alliance, the Horizon Europe programs including the Green Deal Calls, the Innovation Fund or the European Investment Bank to help to accelerate the points 7.-9.

______________________________________________________________________

[1] The national carbon footprint refers to all CO2 emissions: ETS and non-ETS sector emissions together

[2] Data of 2018

[3] https://ec.europa.eu/transport/infrastructure/tentec/tentec-portal/site/en/maps.html; Luxem-bourg lies on the North Sea – Mediterranean route

[4] Estimation based on diesel volumes sold to trucks only in 2018 on Luxembourg’s highway fuel-stations; source FEDIL Groupement Pétrolier

[5] Norsk e-Fuel to build first commercial plant for hydrogen-based renewable aviation fuel

[6] Quarton, C.J. et al (2018). Power-to-gas for injection into the gas grid: What can we learn from real-life projects, economic assessments and systems modelling? Renewable and Sustainable Energy Reviews, Vol. 98, pp. 302-316;

[7] Source: Sector Coupling in Europe, Bloomberg NEF 2020

[8] Based on the final natural gas consumption on a national level (source STATEC 2018)

[9] Data from Voluntary Agreement, 2018

[10] https://hydrogeneurope.eu/electrolysers

[11] Estimation based on historical data across all renewable sources

[12] Over 80% of the electricity in Luxembourg’s grid is sourced from Germany, which has embedded 500gCO2/kWh (source: Moro, A., Lonza, L., Electricity carbon intensity in European Member States: Impacts on GHG emissions of electric vehicles. Transportation Research, Part D: Transport and Environment, Vol 64, Oct. 2018, pp. 5-14)

[13] Hydrogen produced by electricity from Luxembourg’s grid would be nearly 18 times more carbon intensive than blue hydrogen production.

[14] Estimation based on sectoral energy consumptions of 2018

[15] Source: ILR, Chiffre clés du marché de l’électricité 2018 – partie I

[16] Glenk, G., Reichelstain, S. (2019). Economics of converting renewable power to hydrogen. Nature Energy 4: 216-222. https://doi.org/10.1038/s41560-019-0326-1

[17] https://www.spglobal.com/platts/en/market-insights/latest-news/electric-power/092719-green-hydrogen-faces-high-hurdles-massive-potential-irena-report

[18] The national carbon footprint refers to all CO2 emissions: ETS and non-ETS sector emissions together